Cryptocurrency and Islam

Shabana Hasan

.

الأربعاء نوفمبر ٢٩, ٢٠١٧

. Knowledge

Picture Credits: Virtual Reality Times

Islam which is the world’s second-largest religion is also the fastest growing religion in the world. Presently there are approximately 1.6 billion Muslims in the world comprising about 23 percent of the world’s population. Islam offers its own unique banking and finance popularly known as Islamic Banking and Finance. This growing financial system is based on fundamentals which originated from the Holy Quran and ahadith where activities involving riba’ (interest), gharar (uncertainty) and maysir (gambling) are strictly forbidden. As the Islamic Banking and Finance Industry continues to grow, more innovations will take place, and one of the recent innovations that have taken the world by storm amongst others include the developments around blockchain such as cryptocurrencies.

What is Cryptocurrency and what do Islamic scholars think about it?

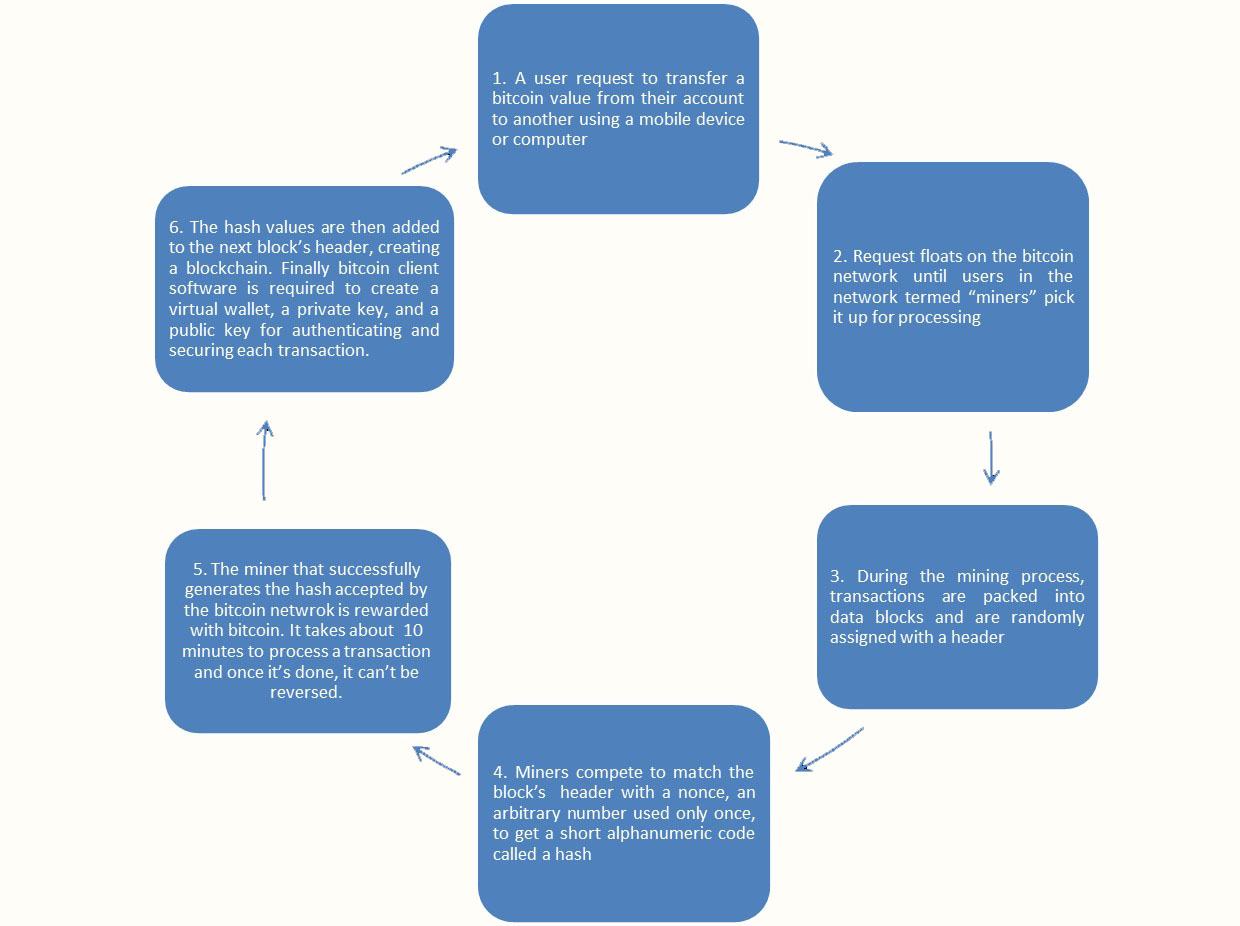

Cryptocurrency is a medium of exchange, created and stored electronically in the blockchain, using encryption techniques to control the creation of monetary units and to verify the transfer of funds. It has no physical form and no central authority or middlemen that control it. Bitcoin is the best known example of cryptocurrency, comprising the bulk of the market share, at 60.8%. Bitcoin is a digital currency that enables payment in a decentralised peer-to-peer (P2P) network that is powered and approved by the consensus of its users. The complete process of how bitcoin works has been outlined below.

To understand whether Islam permits the usage of bitcoin, it will be assessed from four angles namely value of money, payment network method, concept of gharar and serving the real economy. For value of money, Islam deliberates on three elements, namely mal (wealth), taqawwum (legal value) and thamaniyyah (monetary usage). Upon analysing the features of bitcoin, it tends to possess both the features of mal and taqawwum, but not thamaniyyah. Therefore from the perspective of money in Islam, bitcoin probably misses the mark. However from the payment network method, bitcoin can be deemed as halal (permissible) as its practices tend to go beyond what conventional banking can offer. Unlike modern money, bitcoin is not based on debt but instead it is based on proof of payment. On the flipside, being rather volatile in the past leading to price speculation and with no authoritative central body, elements of gharar do exist. This contradicts with one of the main pillars of Shariah compliance. Hence, for bitcoin to be halal, investors and users must understand the risks involved before purchasing them and form an action plan for the possibility of bitcoin failures. Finally from the perspective of serving the real economy, it is noted that the current uses of bitcoin and cryptocurrency investments do not serve the real economy, and do not promote the real growth of an economy.

However, as global cryptocurrency, blockchain etc. is rising and expanding into Muslim-majority markets such as the Middle East, Indonesia, Malaysia and other predominantly Muslim regions, various forms of Shariah-compliant social cryptocurrency, blockchain etc. are fast emerging. For example Jeddah-based Islamic Development Bank (IDB) intends to drive development and financial inclusion in its member countries using a blockchain-based financial instrument. IDB is building a use case using blockchain smart contracts to create Muslim-friendly financial products. Apart from Saudi Arabia, Dubai has also begun the process of developing its own encrypted digital currency for nationwide implementation. Even though the UAE Central Bank have warned in the past against the use of bitcoin due to high propensity for abuse and lack of regulation, the Emiratis appreciate the convenience and urgent need for a digital economy.

It is noteworthy to point out that presently there is no consensus of opinion among Islamic scholars on whether cryptocurrency and peer-to-peer payment systems like bitcoin are Shariah-compliant. Instead, there is still an ongoing debate on this matter. Although the view that its usage is forbidden from an Islamic perspective are not set in stone, at the moment the Islamic Banking and Finance Industry should not consider its use in exchange unless there is a specific need until a regulated and transparent framework is established. Finally the above article is just based on opinions and views on bitcoin, and by no way a final statement or fatwa on this issue.

Shabana Mahmoodul Hasan is a freelance writer on Islamic Banking and Finance.